The single greatest factor to affect your financial goals for retirement has nothing to do with investment options, asset allocations, bonds or stocks. Rather, it’s the amount you save for retirement year over year. And yet, many struggle to save for retirement despite the facts. Business Insider recently published an excellent article that detailed some of the reasons why individuals are not saving enough for retirement.

So now you know why you aren’t saving enough, here are a few top strategies you can use to improve how you save for retirement:

1) Aim to save about 10% of your gross pay for retirement. It’s a rule of thumb – if you’re starting to save later in life, that rate will have to be higher.

2) Double check that you are taking advantage of matching programs with your employer’s 401k.

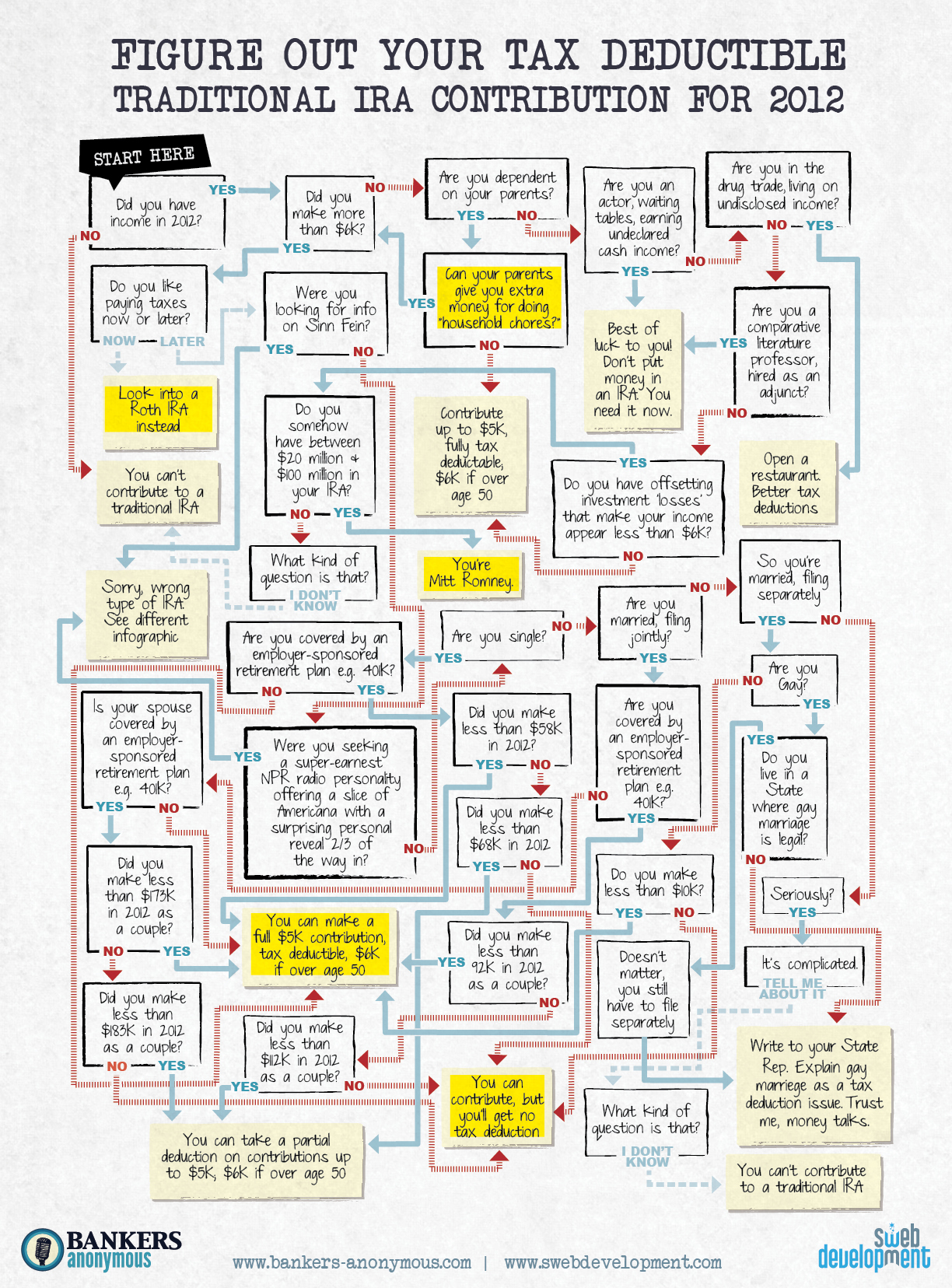

3) Save in addition to your 401k contributions. Just because you’ve maxed out your matching contribution, doesn’t mean that you should stop there. Consider opening a Roth IRA to save more.

4) Track expenses. To reiterate one of the tips in the article, by reducing how much you spend on non-essential expenses you can end up with a nice contribution to your retirement accounts. You can track expenses yourself or use a site like mint.com

5) Set up systematic contributions. It’s very easy to link your checking account to your retirement account and have contributions made to your investment account automatically. You can even explore the option of a payroll deduction.

Regardless of the strategy you adopt, remember that it will require self control. It’s very easy to shift dollars you earmarked for retirement to pay for that unexpected expense. Develop a plan, stick to it and review it periodically.