Congratulations – You graduated from college and landed your first job. Unfortunately, the party ends shortly after that. According to Zillow, 22.5% of millennials ages 24-36 live at home (roughly 12 million). And of those “Boomeranger”, only 12.5% are unemployed, indicating that the majority choose to stay home for one reason or another. The cause of this could be a number of reasons such as rising costs or low wages. Not to mention crushing debt from student loans and credit cards.

For people just getting out of school and starting to establish themselves, here are six important concepts to keep in mind:

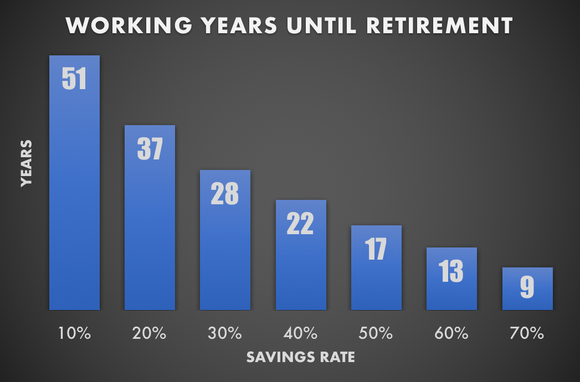

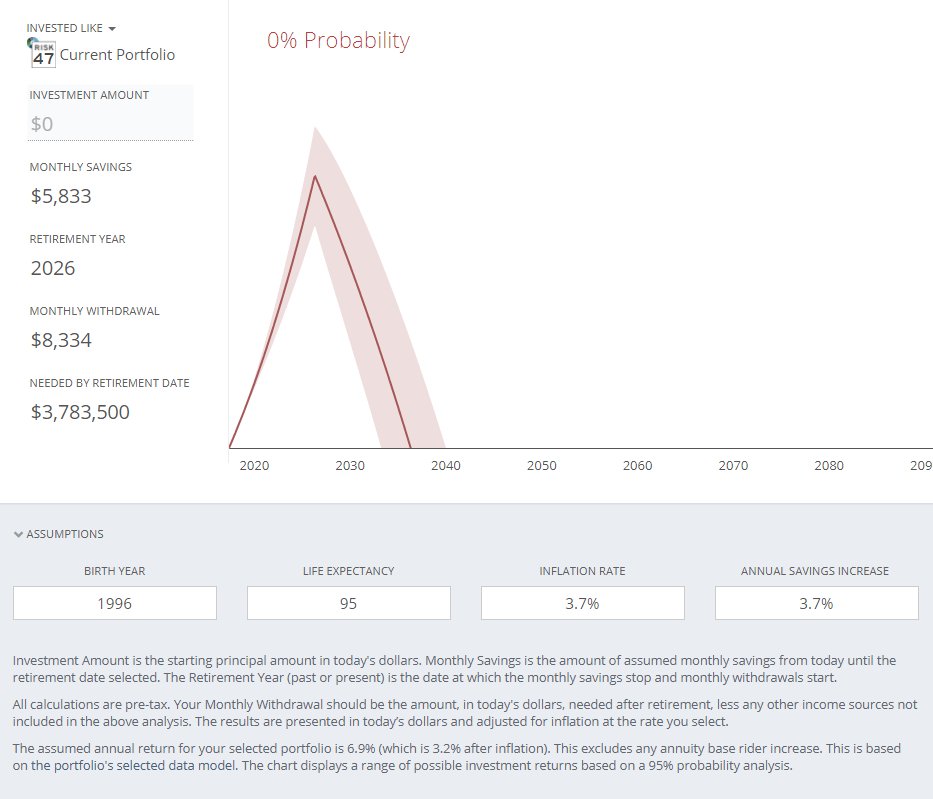

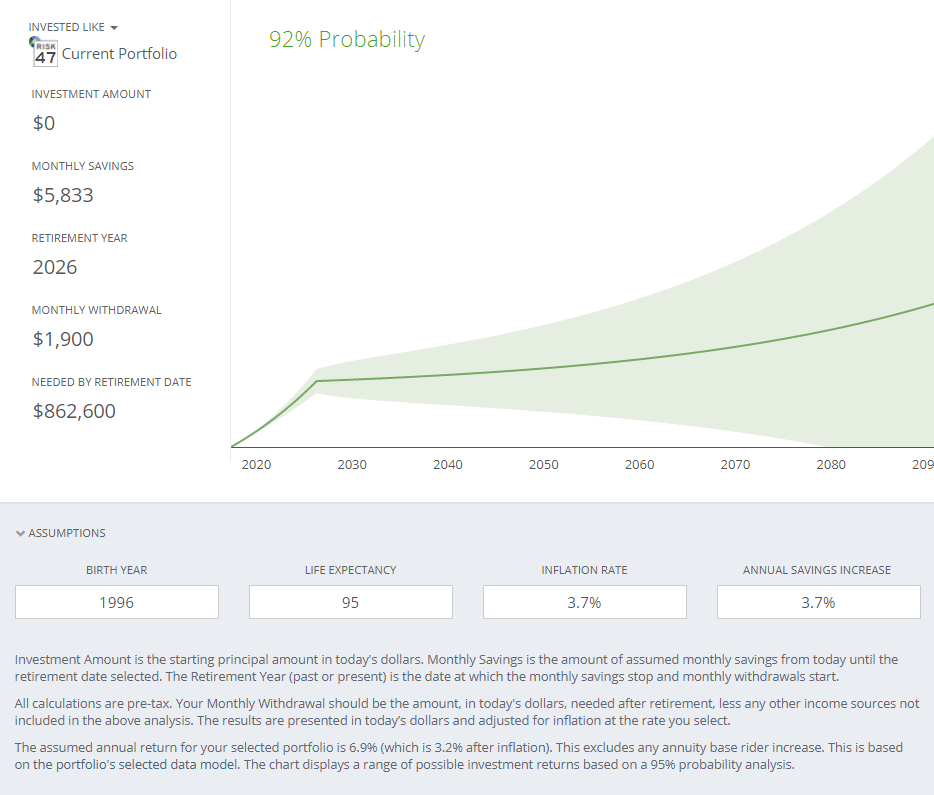

1. Automate your savings: Set realistic goals. Starting small with automated savings is a good place to start, in that case, you won’t feel strapped for cash and it’s much less painful. For example $5 a week. Once you get more comfortable with saving money increase it in smaller increments. Use any number of tools that will do it automatically for you. So you can “save-and-forget”. Over time, you can slowly raise the amount. Starting early and being consistent can have huge implications later in life.

2. Design a budget: Learn from your college years. When it came down to entertainment purchases or gas for your car, it was an easy choice. But now, life is more complicated. You have to save for big expenses (like replacing a car in a few years), paying down debts, and saving for retirement (which seems absurdly far away for a recent grad to consider). The solution is a budget. Start by paying yourself first. By that, I mean save for your future (retirement and major expenses). Then, budget out your most essential day-to-day expenses. Whatever is left can be spent on discretionary expenses (eating out, having fun, etc).

3. Search for less expensive alternatives: Building on the budget concept, there are simple ways to cut costs. Maybe there is a gym in the area $10 less per month, those savings can add up quickly. Review your subscriptions, search for alternatives and calculate the potential savings. Subscriptions have grown in popularity over the last ten years. You’d be surprised how much you can save by eliminating a few subscriptions or finding a cheaper option.

4. Beware of ‘Advertiming’: You’ve just reached a major milestone in your life, and brands also realize that. In fact, they’ve gotten pretty smart. Advertiming is a strategy used in advertising to run adverts to a specific audience at a specific time, (i.e Dunkin Donuts ads during the morning rush hour, AARP magazine in the mail when you turn 50). Audi offers a “College Graduate Offer” for recent grads, they’re trying to hook you early.

5. Don’t buy a brand new car after landing your first job: JD Power discovered that 29% of new vehicles are bought by Millennials. Recent grads might be experiencing the income effect. Imagine going from a college student budget and meal plans to a salary, you feel a whole new level of freedom. It’s important to recognize that the income effect is just an emotional reaction to a major increase in cash flow. You’re not used to it yet.

Kelley Blue Book’s most recent figure for the average price of a new car is $35,285. If the average depreciation of a car is 20% after the first year you should rethink your options. The need for a reliable car could be validated, but that could also be $7,057 towards paying off lingering debt. Instead look for a New-Used car.

6. Ease off the social media: Recent data from Forbes suggests 72% of Millennials have made fashion and beauty purchases influenced from Instagram posts alone. Could the social influence be thinning their wallets? At the very least, it’s important to keep in mind how deeply the consumer culture has worked its way into apps we use every day (like Facebook and Instagram)

Like generations before them, millennials attempt to leave the nest while burdened with rising costs of living, peer pressures and debt. Brands are getting smarter with targeting them at a time when they’re not financially secure to pursue their expensive tastes. Needs for short-term appear more important than the long-term. In essence, it comes down to needs vs. wants. The ability to distinguish between the two is a simple, timeless concept, yet so often overlooked.

Budget, plan, ignore the noise and most importantly, prioritize.

Special thanks to Dan Varghese, our current intern for researching this post.